HDFC Bank (NS:HDBK) recently unveiled its quarterly performance, showcasing a notable upswing with core Pre-Provision Operating Profit (PPOP) growth of 3% quarter-on-quarter (QoQ). Impressively, the bank's core PPOP-Return on Assets (ROA) and ROA stood at approximately 2.6% and 1.9% respectively, aligning closely with Goldman Sachs (NYSE:GS)' estimations.

As the quarter unfolded, HDFC Bank strategically focused on three key areas: deposit momentum, loan-deposit ratio, and net interest margins. Despite challenging macroeconomic conditions, the bank effectively addressed these focal points. Noteworthy achievements include a substantial increase in deposit market share by 17% in Q4 compared to the previous quarter, coupled with an enhancement in Current Account Savings Account (CASA) ratio by 140 basis points to approximately 29%.

Furthermore, HDFC Bank bolstered its loan-to-deposit ratio by around 600 basis points to reach 104%, while simultaneously elevating the Liquidity Coverage Ratio (LCR) by 500 basis points to 115%. Surpassing expectations, the bank also saw a marginal improvement in margins by 4 basis points, defying anticipated contraction due to an unfavorable asset mix.

Goldman Sachs' interactions with investors revealed a varied range of earnings per share (EPS) outcomes. While sell-side estimates fluctuated between INR 87-101, the buy-side estimate settled around INR 90. Despite this diversity, Goldman Sachs anticipates a convergence of these expectations post-management commentary.

Looking ahead, Goldman Sachs anticipates HDFC Bank to undertake strategic initiatives aimed at driving growth and profitability. These include controlling deposit costs, optimizing lending rates, and capitalizing on operating leverage. Notably, the bank's potential reduction in loan growth aims to enhance focus on lucrative opportunities amidst competitive and uncertain market conditions.

Additionally, HDFC Bank's proactive measures, such as the increase in Priority Sector Lending (PSL) loans and productivity enhancements in branches, underscore its resilience and adaptability.

Goldman Sachs maintains a positive outlook on HDFC Bank, emphasizing its robust performance and strategic foresight. With a projected rebound in core PPOP-ROA and accelerated growth prospects, HDFC Bank stands poised for continued success. As such, Goldman Sachs reiterates a Buy rating on HDFC Bank, foreseeing a compelling upside potential of 27%.

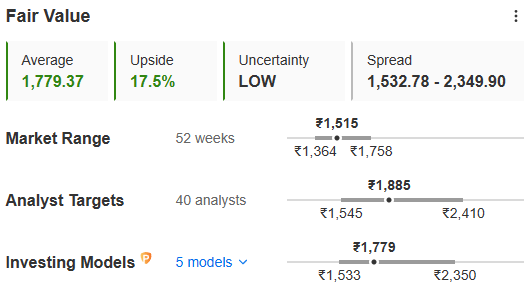

Image Source: InvestingPro

But how can you track the average consensus of all analysts covering HDFC Bank or any other stock for that matter? The easiest way is to head to InvestingPro where the aggregate of all analysts’ targets is taken into consideration and a mean is taken to depict the average consensus of all of them.

The analysts’ target range is also there to help investors gauge the variability in opinions of the street. This not only helps to make decisions regarding investments but also helps to curb the risk.

A total of 40 analysts have their coverage on HDFC Bank and have given targets ranging from INR 1,545 per share to INR 2,410 per share, with an average of INR 1,885 per share.

And to know the true intrinsic value of the stock, investors can always refer to the fair value section which gives an accurate representation of the valuation status of the counter. In the case of HDFC Bank, after analyzing it from 5 financial models, the fair value comes at INR 1,779 per share, a good 17.5% upside from the CMP

Unlock the power of InvestingPro at an incredible 69% discount, now just INR 216/month for a limited time! Access comprehensive stock analysis, track major analysts’ targets and know the intrinsic value effortlessly to make informed investment decisions. Don't miss out on this exclusive offer – subscribe to InvestingPro today by clicking here!

X (formerly, Twitter) - Aayush Khanna