Rates Spark: Range Trading Within a Declining Channel

ING Economic and Financial Analysis | Apr 18, 2023 17:56

Markets are still waiting for the data smoking gun that proves that a recession is coming and that inflation is a problem of the past. Until then, rates should continue to rise toward the top of their range, but we doubt they will match their early-March highs.

Room for one more technical 'head fake' into the May Fed meeting

The growing confidence that contagion risk among US regional banks is now manageable, combined with the (probably misplaced) hope that recent stress will have limited real economic impact, are a toxic cocktail for core bonds. This is the last week before the Fed’s pre-meeting quiet period and recent comments have done nothing to contradict the market’s growing conviction (over 90%) that at least one more 25bp hike will be delivered.

We do not change our view that rates are on a downward path but we also reiterate that this adjustment will not be on a straight line. Realized and implied volatility remain elevated, and the coming weeks and months will feel a lot like range-trading, but within a declining channel. At least until data takes a more decisive turn for the worse. This is the last week before the Fed’s pre-meeting quiet period

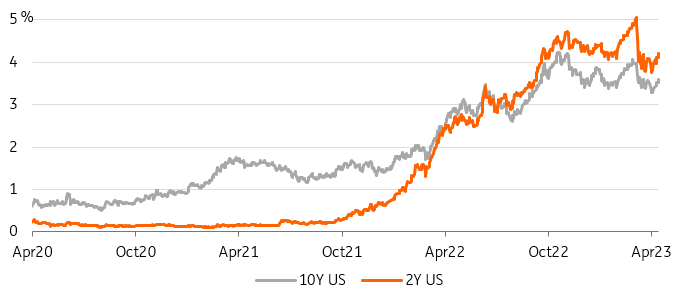

If front-end bonds are the worse affected, the sell-off in longer-dated treasuries has also been significant. Both 2Y and 10Y yields are standing at or above their post-Silicon Valley Bank (SVB) failure highs. These levels should, in theory, act as a psychological barrier to further rises unless investors are happy to move on from the US regional banking crisis without materially changing their economic expectations. To us, this is a stretch. Access to credit was already showing signs of tightening even prior to SVB’s failure.

US yields are at their highest levels since early March

Source: Refinitiv, ING

More reasons to believe in 'higher-for-longer' in Europe

If the recent re-pricing higher in rates very much feels like it is US-led, we think euro rates actually have a better reason to rise. According to a Bloomberg survey, the consensus among economists is that the European Central Bank will deliver three more 25bp hikes in this cycle, which also ties in with what the swap curve implies. One could, of course, point out that with only one more hike currently priced by the US curve this year, followed by two cuts, there is more room for US rates to rise in the near term as optimism rises. We agree, but think this wouldn’t be sustainable.

Get The App

Join the millions of people who stay on top of global financial markets with Investing.com.Download NowConsensus among economists is that the ECB will deliver three more 25bp hikes in this cycle

Fundamentally, the discount for more hikes in Europe is the result of the ECB’s later start to its hiking cycle, but also of still accelerating core inflation. Barring a drastic divergence between the two economies, to Europe’s disfavor, it makes much more sense for European markets to believe in the higher for longer narrative than in the US, where rates are already twice what the Fed signals is the long-term neutral rate. Plentiful long-end supply probably aggravated the euro bond sell-off in recent days, and we could see some stabilization today. This means wider Treasury-Bund spreads before the tightening resumes.

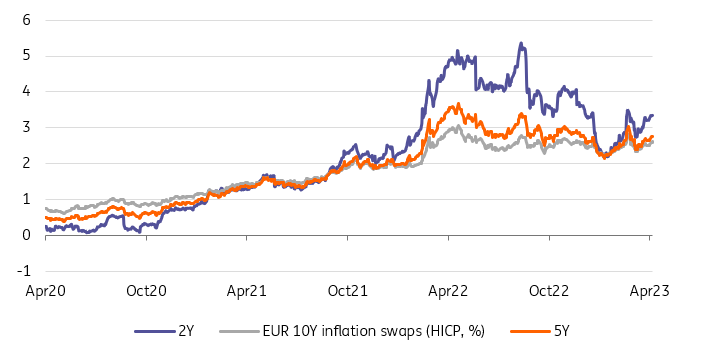

European inflation swaps are on the rise again

Source: Refinitiv, ING

Today’s events and market view

There is a decent amount of bonds on offer today, especially at the long end. Austria mandated banks for the sale of a dual-tranche 6Y green bond and 30Y conventional bond via syndication. This will add to scheduled sales from the Netherlands and the UK, also in the 30Y sector.

Finland has planned sales in 10Y and 24Y maturities. Most of the detrimental effect on bonds direction should have been felt already, but we think continued optimism about the economy after improving Chinese growth in Q1 skew yields higher today.

European data of note include the April Zew survey and European trade balance for February. US economic releases will mostly relate to the housing sector with housing starts and building permits to look out for.

Disclaimer: This publication has been prepared by ING solely for information purposes, irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.